Houston Business Owners Policy

Your core coverage is bundled. The exclusions decide what needs its own policy.

A business owners policy bundles general liability, property, and business income. Workers comp, commercial auto, cyber, and professional liability are not in the package. We read what the policy includes and what it leaves out, before a claim, not after.

Business Owners Policy, The McDade Way

A business owners policy is the most common commercial product in Texas, and the one most often mistaken for complete coverage. It bundles general liability, property, and business income. It does not bundle workers comp, commercial auto, cyber, or professional liability. We translate the contract before claim time, so what the package leaves out does not become your problem at the worst moment.

Six things in. And four major things still missing.

Bundled: General Liability

Third-party bodily injury and property damage from operations and premises. Per-occurrence and general aggregate limits. Standard ISO CGL form CG 00 01 applies. Additional Insured endorsements available by request and contract requirement.

Bundled: Commercial Property

Buildings, business personal property, equipment, and inventory. Texas Wind/Hail percentage deductible (1 to 5 percent of building value) applies. Coinsurance compliance required. Ordinance or Law and Equipment Breakdown often included as basic endorsements.

Bundled: Business Income

Lost net profit plus continuing operating expenses during the period of restoration after a covered property loss. 12-month default period of indemnity with extension endorsements available. Extra Expense coverage typically included.

Excluded: Workers Compensation

Always sold as a separate policy. Texas employers can be subscribers (carrying WC) or non-subscribers (forgoing WC and losing tort immunity). McDade evaluates Texas WC alongside the BOP.

Excluded: Commercial Auto

Always sold separately. Vehicles used in business operations require a commercial auto policy. Hired and Non-Owned Auto (HNOA) coverage is critical for businesses with employees driving personal vehicles for work.

Excluded: Professional Liability and Cyber

Professional Liability is almost always excluded from BOPs. Cyber coverage on BOPs typically caps at 25,000 to 100,000 dollars, insufficient for the realistic 120,000 to 1,240,000 dollar SMB breach range. Both require stand-alone policies.

Texas BOPs carry Texas property exposures. And Texas eligibility maps.

Texas Business Owners Policies operate within the Texas commercial property and liability framework. The Texas-specific factors that decide whether a BOP is the right structure for a Texas business include eligibility class mapping, Texas wind and hail exposure, coinsurance compliance, and the gap-fill program around the BOP package.

Something Powerful

Tell The Reader More

The headline and subheader tells us what you're offering, and the form header closes the deal. Over here you can explain why your offer is so great it's worth filling out a form for.

Remember:

- Bullets are great

- For spelling out benefits and

- Turning visitors into leads.

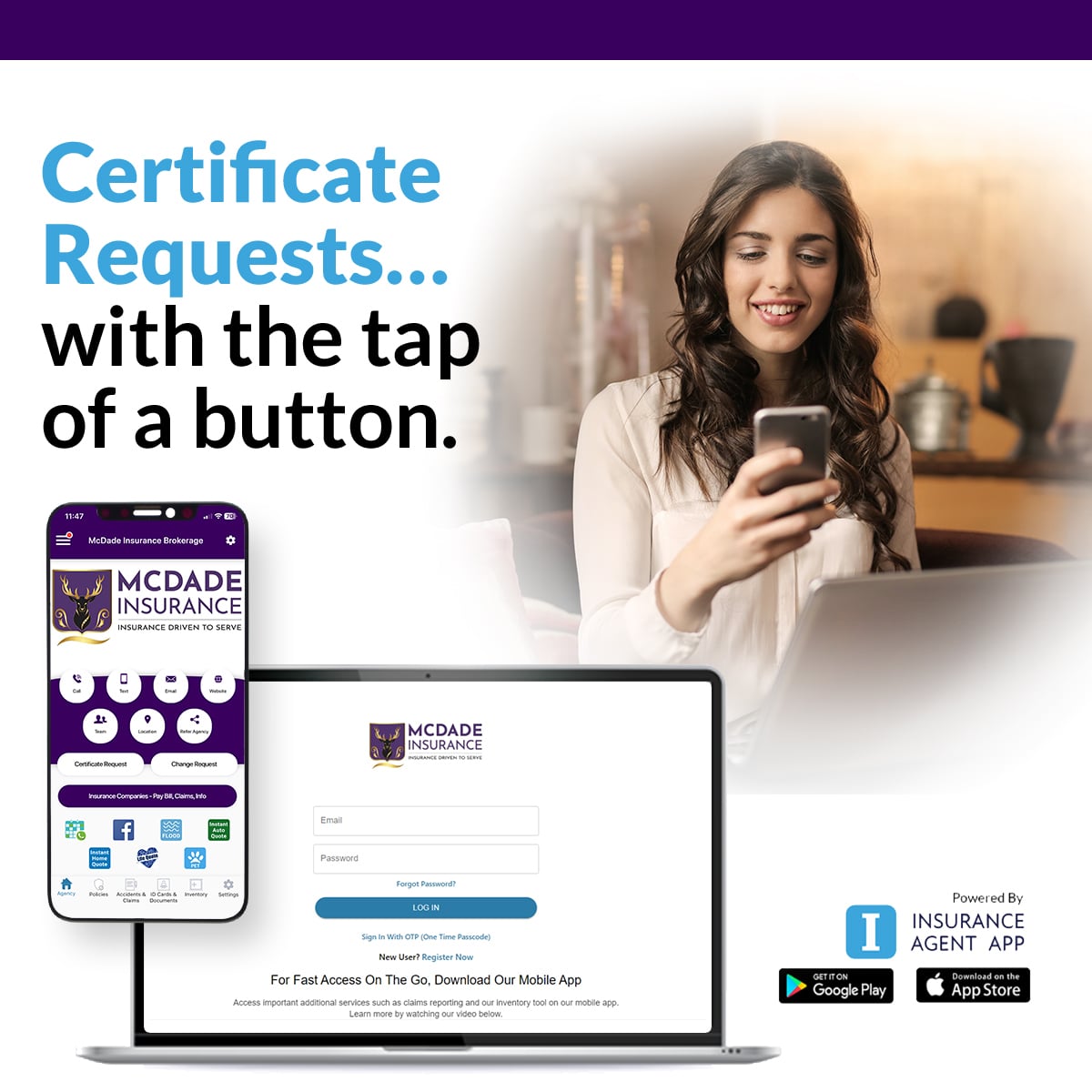

Your COIs. On Your Phone.

McDade clients get instant access to certificates of insurance from a mobile app. Issue. Email. Manage. No phone tag. No waiting on email.

Issue COIs on demand from your phone, anywhere, 24/7.

Email certificates directly to general contractors, vendors, or job sites in seconds.

Manage active certificates and policy info in one place.

Issue Certificates from your phone. The agency stays at the center.

If your business gets a certificate of insurance request twice a week, the McDade Client App removes that bottleneck. Pull an active certificate showing GL and property coverage from your BOP, edit the certificate holder, and email the COI to a general contractor, vendor, or job site directly from your phone in seconds. Free to McDade clients. SOC 2 Type II compliant.

Certificates on Demand

Issue COIs showing your BOP coverages in seconds.

Auto ID Cards

Current commercial auto ID cards on your phone for traffic stops.

Mobile Claims Kit

Document property losses and claims from the scene with photos.

Direct McDade Contact

Tap to call Dallas Downey or the McDade service team.

Built on the Insurance Agent App platform by GoInsuranceAgent, a Vertafore Orange Partner.

SOC 2 Type II compliantA BOP sits in a portfolio. These four sit alongside it.

Texas Workers Compensation

Statutory employee injury benefits in exchange for tort immunity. Texas is the only state where WC is optional, but most BOP-eligible businesses subscribe.

Commercial Auto

Auto liability and physical damage for vehicles used in business. Hired and Non-Owned Auto endorsement critical for businesses with employees driving personal vehicles for work.

Professional Liability (E&O)

Claims arising from professional services and advice. Required for IT services, accounting, legal, consulting, real estate, financial advisory, design professionals, and any service-providing business.

Cyber Liability

First-party and third-party cyber coverage. The BOP's 25,000 to 100,000 dollar cyber endorsement is insufficient given the 120,000 to 1,240,000 dollar realistic SMB breach range. Stand-alone cyber is the answer.

Business Owners Policy. Read the questions worth asking.

What is a Business Owners Policy and what is bundled inside it?

A Business Owners Policy, or BOP, is a packaged commercial insurance product that bundles General Liability, Commercial Property, and Business Income coverage into a single policy at a single premium. The package typically includes Commercial General Liability with per-occurrence and general aggregate limits, Commercial Property with Building and Business Personal Property coverage, Business Income (Interruption) coverage with a stated period of indemnity, and some Equipment Breakdown coverage. Most Texas carriers offer BOPs through the Insurance Services Office BOP form (BP 00 03) with carrier-specific eligibility classes and endorsement variants. The BOP package is meaningfully less expensive than buying General Liability and Commercial Property as separate policies for the same coverage, and is the most common Texas commercial insurance product for businesses meeting the eligibility threshold.

What is NOT bundled in a BOP and where are the most common Texas gaps?

The BOP package does not include several commercial coverages that most Texas businesses need. Workers Compensation is always sold as a separate policy. Commercial Auto is always sold separately. Professional Liability (Errors and Omissions) is sold separately for service businesses. Cyber Liability is sold separately and is increasingly mandatory for businesses handling customer data. Umbrella and Excess Liability sits above the BOP and is sold separately. Employment Practices Liability (EPLI) covering harassment, discrimination, and wrongful termination is often a separate endorsement or stand-alone policy. Pollution Liability is excluded from most BOPs. Liquor Liability is excluded from most BOPs. The most common Texas BOP gap is a small business buying a BOP and assuming everything commercial is covered, then discovering at claim time that the actual loss falls under one of the excluded coverages.

What businesses qualify for a Business Owners Policy in Texas?

Most Texas BOP carriers use eligibility rules tied to class code, revenue, payroll, property values, claims history, occupancy, and operational hazard. The question is not whether a BOP is good or bad; it is whether your current operation still fits the BOP box and whether the excluded exposures are handled elsewhere. The McDade Review compares those eligibility rules across available carriers.

How does the Texas Wind/Hail percentage deductible apply on a BOP?

Texas BOPs apply the same Texas Wind/Hail percentage deductible as stand-alone Commercial Property policies. The deductible typically ranges from 1 to 5 percent of the building value (not the loss amount) and applies to wind and hail losses separately from the standard flat deductible on other property losses. A Texas BOP covering a 500,000 dollar building with a 2 percent wind/hail deductible carries a 10,000 dollar out-of-pocket exposure on every wind or hail loss. Texas Wind/Hail percentage deductibles are not optional for most coastal and hail-corridor Texas counties. The McDade BOP Review evaluates the percentage and the carrier-specific roof endorsement variant on every Texas BOP.

How does coinsurance work on a BOP?

Most Texas BOPs include a coinsurance clause that requires you to insure to a stated percentage (typically 80, 90, or 100 percent) of the building's replacement cost. If actual insured value falls short of the required percentage at the time of a partial loss, the carrier reduces the claim payment proportionally by the underinsurance ratio. Some Texas BOP carriers offer Agreed Value endorsements that waive the coinsurance penalty when the insured value is documented and accepted at policy inception. The Agreed Value endorsement is a McDade Review checkpoint because coinsurance penalties surface at claim time, not renewal time. A Texas business insured at 70 percent of building replacement cost when 80 percent was required collects 87.5 percent of any covered loss, not the full claim amount.

What is Business Income coverage on a BOP and what limit do I need?

Business Income (Interruption) coverage on a BOP pays lost net profit plus continuing normal operating expenses during the period of restoration after a covered property loss. Coverage typically begins 72 hours after the loss (the waiting period) and continues until the property is restored or for the stated period of indemnity (12 months default, with extensions up to 24 or 36 months available by endorsement). Calculating the Business Income limit requires a 12-month projection of net profit plus continuing expenses (rent, utilities, payroll for key employees, debt service, insurance, taxes) and is the area most often underestimated on Texas BOPs. Extra Expense coverage pays the additional cost to minimize the Business Income loss, including temporary location rent, expedited shipping, temporary equipment rental, and overtime payroll. The McDade BOP Review evaluates Business Income limits against current revenue and operating profile.

Does a BOP include Cyber or Professional Liability coverage?

Most Texas BOPs do not include meaningful cyber or professional liability coverage. Some BOP carriers offer a small cyber endorsement, typically with limits between 25,000 and 100,000 dollars, which can fund initial breach notification but is generally insufficient for any serious cyber incident given that the realistic SMB breach cost range is 120,000 dollars to 1,240,000 dollars per Verizon DBIR research. Professional Liability is almost always excluded from BOPs and must be purchased separately. Texas service businesses (consulting, accounting, legal, IT services, design professionals, real estate, financial advisory) need stand-alone Professional Liability policies regardless of BOP coverage. The McDade BOP Review identifies cyber and professional liability gaps in every Texas BOP review.

When should a Texas business outgrow a BOP and move to a layered commercial program?

A Texas business typically outgrows the BOP package when operations become more complex than the carrier's packaged-policy appetite. That can happen when revenue, payroll, property values, contracts, vehicle use, professional services, cyber exposure, employment practices exposure, or higher-hazard operations move beyond the BOP box. At that point, a layered commercial program with separately rated General Liability, Commercial Property, Business Income, Workers Compensation, Commercial Auto, Cyber, and Umbrella policies may fit better than renewing a package that no longer matches the business.

What is the McDade Business Owners Policy Review?

The McDade BOP Review is an audit of your existing BOP by Dallas Downey, CLCS, with the McDade commercial team. The review evaluates four primary areas. First, the BOP eligibility classification against current operational reality (operations sometimes grow beyond original BOP eligibility without the renewing carrier or the insured noticing). Second, the property limit structure including building values, business personal property, Texas Wind/Hail percentage deductible, coinsurance compliance, and Agreed Value endorsement. Third, the Business Income limit, period of indemnity, and Extra Expense limit against current 12-month projection of net profit and continuing expenses. Fourth, the coverage gaps the BOP package does not address (Workers Compensation, Commercial Auto, Professional Liability, Cyber, EPLI, Umbrella) and whether the broader commercial program adequately fills each. About 40 percent of the time the review confirms the current BOP and broader program are correct. The other 60 percent identifies eligibility, limit, or gap-fill opportunities.

Who handles Business Owners Policies at McDade?

Dallas Downey, CLCS leads the McDade commercial insurance team including the Business Owners Policy product. Dallas holds the Certified Lines Coverage Specialist designation and routes commercial conversations through a dedicated commercial meeting calendar. The McDade office serves the Houston metropolitan area including Spring, Klein, Tomball, Cypress, The Woodlands, Conroe, Humble, Katy, and Bridgeland, plus all of Texas through Premier Group Insurance carrier access including 50+ top Texas carriers we know well. McDade Insurance Brokerage Group is licensed by the Texas Department of Insurance (Texas License 2539471). Schedule a commercial review with Dallas through the commercial routing on this page or call the McDade office at 281.378.5002.

What Texas business owners say.

Real Google reviews from the Texas business owners and commercial clients the McDade team serves across Houston and the wider metro.

Send your current BOP declarations. Dallas Downey audits all four.

The McDade BOP Review evaluates the BOP eligibility classification against current operational reality, the property limit structure including Texas Wind/Hail percentage deductible and coinsurance compliance, the Business Income limit and period of indemnity against current revenue, and the coverage gaps the BOP does not address (Workers Compensation, Commercial Auto, Professional Liability, Cyber, EPLI, Umbrella). Dallas Downey, CLCS leads the review. Most reviews complete inside one business week. About 40 percent of the time the audit confirms the current BOP and broader program are correct. The other 60 percent identifies eligibility, limit, or gap-fill opportunities.

Back to the commercial hub. Houston Business Insurance

Or call 281.378.5002

The review is advisory. McDade is licensed by the Texas Department of Insurance (Texas License 2539471).