Houston Professional Liability Insurance

Your work is covered. The retroactive date decides how far back.

Claims-made triggers, retroactive dates, defense inside or outside the limit, and the exclusions decide what an E&O claim pays. We read all of it with you before a claim, not after.

Professional Liability/ E & O, The McDade Way

The terms that decide an E&O claim are set long before the dispute. The claims-made trigger, the retroactive date, whether defense costs sit inside or outside the limit, and the exclusions written for your profession. We translate the contract before claim time, so the policy you renewed is the policy that answers when a client points a finger.

Six clauses. And the retroactive date that overrides all six.

Claims-Made Trigger

Policy responds based on when the claim is reported, not when the alleged error occurred. Continuous coverage required for value. A lapse in coverage breaks the chain and exposes all prior work to uncovered claims.

Retroactive Date

The earliest date for which the policy will cover incidents. Claims from work performed before this date are not covered regardless of when reported. Should be preserved (not reset forward) at carrier changes. The most-missed Texas E&O audit checkpoint.

Defense Cost Structure

Defense Inside Limits erodes the indemnity available for settlement or judgment. Defense Outside Limits preserves the full indemnity. On larger defense matters, this structure decides whether the indemnity limit is preserved or reduced while the case is being defended.

Tail Coverage (Extended Reporting Period)

Extends the claim reporting window after policy termination. Typically 100 to 150 percent of annual premium for unlimited tail. Critical at retirement, business sale, or carrier change. Some carriers offer free 30 to 60 day automatic tails.

Prior Acts Coverage

When changing carriers, prior acts coverage on the new policy preserves the retroactive date of the prior policy, maintaining continuous coverage chain. Without prior acts, the new retroactive date typically resets to the new policy effective date, creating exposure.

Profession-Specific Exclusions

Each profession faces specific exclusions. Common exclusions include the regulatory exclusion, the prior knowledge exclusion, the contractual liability exclusion, the dishonest acts exclusion, and the bodily injury exclusion. Profession-specific exclusions for IT services, healthcare, design professionals, and financial advisors require specific evaluation.

Texas E&O is shaped by Insurance Code, DTPA overlap, and Stowers.

Texas Professional Liability operates under the Texas Insurance Code, the Texas Civil Practice and Remedies Code, and Texas case law on professional negligence claims by industry sector. The Texas Department of Insurance regulates professional liability carriers in Texas.

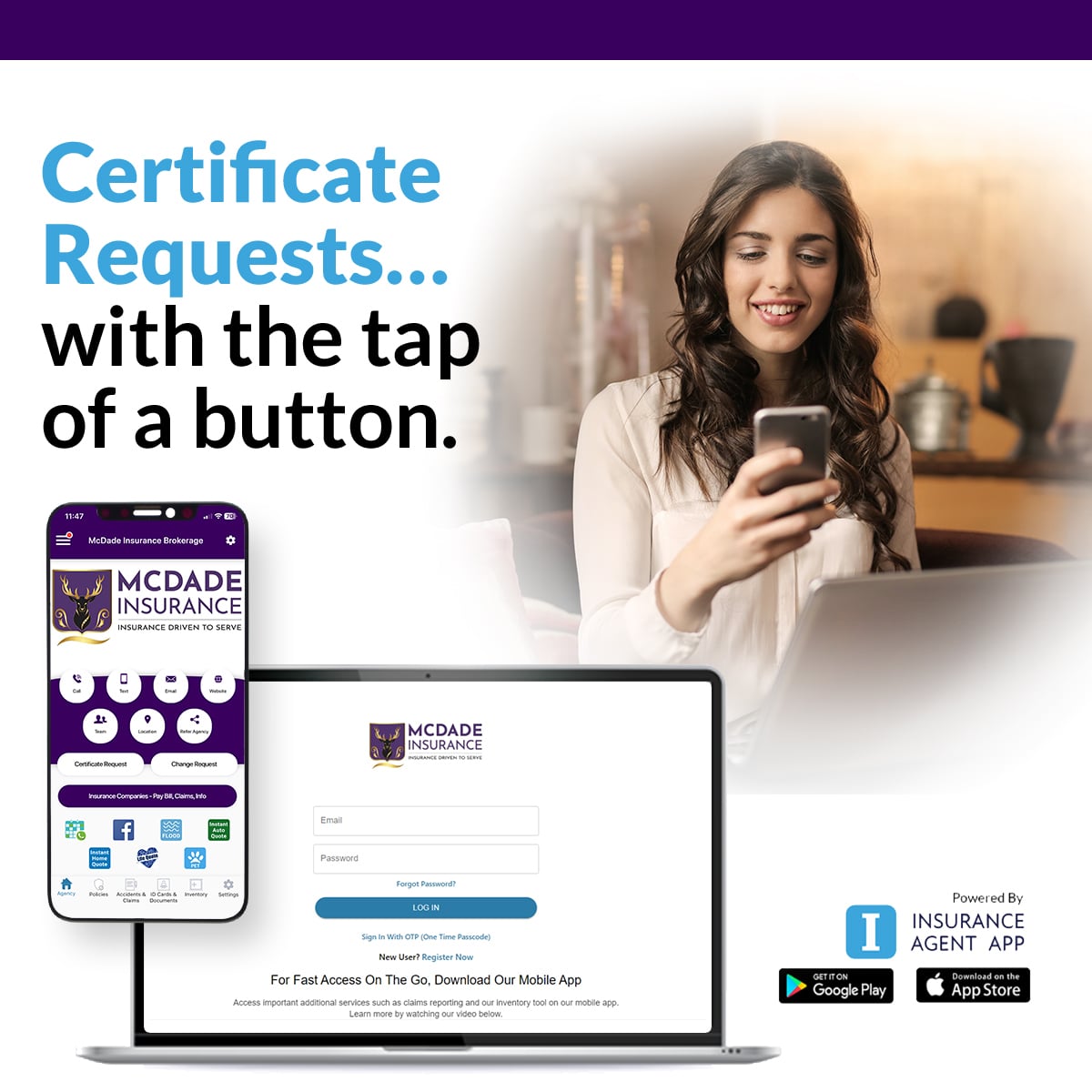

Your COIs. On Your Phone.

McDade clients get instant access to certificates of insurance from a mobile app. Issue. Email. Manage. No phone tag. No waiting on email.

Issue COIs on demand from your phone, anywhere, 24/7.

Email certificates directly to general contractors, vendors, or job sites in seconds.

Manage active certificates and policy info in one place.

Issue Certificates from your phone. The agency stays at the center.

If your professional services firm gets a certificate of insurance request twice a week, the McDade Client App removes that bottleneck. Pull an active certificate showing professional liability, edit the certificate holder, and email the COI to a client or contracting party directly from your phone in seconds. Free to McDade clients. SOC 2 Type II compliant.

Certificates on Demand

Issue COIs showing E&O and commercial coverage in seconds.

Auto ID Cards

Current Texas auto ID cards on your phone for traffic stops.

Mobile Claims Kit

Document client matters and claim notifications from the field.

Direct McDade Contact

Tap to call Dallas Downey or the McDade service team.

Built on the Insurance Agent App platform by GoInsuranceAgent, a Vertafore Orange Partner.

SOC 2 Type II compliantProfessional Liability sits in a portfolio. Here is what sits next to it.

General Liability

Third-party bodily injury and property damage. GL explicitly excludes professional liability. The two policies sit next to each other and do not overlap. Service businesses need both.

Cyber Liability

First-party and third-party cyber coverage. For IT services firms, sometimes bundled with E&O in a single technology professional liability policy. McDade audits the bundling structure.

Business Owners Policy (BOP)

Packaged GL and property for small and mid-size businesses. BOPs almost always exclude professional liability. Stand-alone E&O is the answer for service businesses.

Employment Practices Liability (EPLI)

Harassment, discrimination, and wrongful termination claims by employees. Sits next to E&O for service businesses where employee disputes and client disputes can both arise.

Professional Liability. Read the questions worth asking.

What does Professional Liability insurance cover and what does it cost when claims happen?

Professional Liability insurance, also called Errors and Omissions or E&O insurance, covers claims arising from the professional services your business provides. Coverage applies to allegations of professional negligence, mistakes, errors, omissions, breach of duty, and failure to deliver promised services or advice. Defense costs are typically included within the limit (eroding the limit) or paid in addition to the limit, depending on the policy structure. Defense costs can erode the available limit quickly when they are inside limits, and the cost of defending the allegation may matter as much as the allegation itself. The McDade review checks whether defense is inside or outside the limit and whether the policy structure fits the work you perform.

What is the difference between Professional Liability and General Liability?

General Liability covers third-party bodily injury and property damage arising from your business operations and premises. Professional Liability covers economic loss to third parties arising from your professional services, advice, and work product. The two policies sit next to each other and do not overlap. An architect's General Liability covers a client tripping over a power cord at the architect's office. The architect's Professional Liability covers a client suing because the architect's design produced a structural failure or code violation. An accountant's General Liability covers a client slipping on a wet floor in the lobby. The accountant's Professional Liability covers a client suing because the accountant missed a deduction or misfiled a return. Service businesses generally need both.

What is the claims-made coverage trigger and why is it different from General Liability?

Professional Liability policies are typically claims-made, meaning the policy that responds to a claim is the policy in force when the claim is reported, not the policy in force when the alleged error occurred. This is fundamentally different from General Liability, which is occurrence-based and triggered by when the injury or damage occurred. Claims-made requires continuous coverage to be valuable. If you let a claims-made policy lapse, claims arising from work you performed during the policy period but reported after expiration are uncovered. Tail coverage, also called Extended Reporting Period coverage, extends the reporting window after a claims-made policy ends. Tail coverage typically costs 100 to 150 percent of the annual premium. The McDade Review evaluates the claims-made trigger and tail coverage need on every Professional Liability policy.

What is a Retroactive Date and why does it matter?

The Retroactive Date on a claims-made Professional Liability policy is the earliest date for which the policy will cover incidents. Claims arising from professional services performed before the Retroactive Date are not covered, regardless of when the claim is reported. When you first buy E&O coverage, the Retroactive Date typically equals the policy effective date. When you renew or move to a new carrier, the Retroactive Date should be preserved or moved earlier (prior acts coverage) rather than reset forward. Resetting the Retroactive Date forward creates a coverage gap. Many Texas businesses unknowingly accept a forward-reset Retroactive Date during carrier changes, exposing all prior-year work to uncovered claims. The McDade Review checks the Retroactive Date on every Professional Liability policy.

What is Tail Coverage (Extended Reporting Period)?

Tail Coverage, formally called Extended Reporting Period coverage, extends the claim-reporting window after a claims-made Professional Liability policy terminates. Tail Coverage allows claims arising from work performed during the policy period but reported after the policy expires to still be covered. Tail Coverage is critical when retiring from practice, selling a business, switching carriers, or terminating professional services. Standard Tail Coverage extensions are one year, three years, five years, ten years, and unlimited. Cost typically ranges from 100 to 150 percent of the most recent annual premium for unlimited tail, with shorter tails costing proportionally less. Some carriers offer free 30 or 60 day automatic tail coverage. The McDade Review evaluates Tail Coverage need at every policy change.

Are defense costs paid inside or outside the limit?

Professional Liability policies handle defense costs in one of two ways. Defense Inside Limits means defense costs (legal fees, expert witnesses, court costs) reduce the available policy limit. A 1,000,000 dollar policy with 400,000 dollars in defense costs has 600,000 dollars remaining for settlement or judgment. Defense Outside Limits means defense costs are paid in addition to the limit and do not reduce the available indemnity. The same 1,000,000 dollar policy with 400,000 dollars in defense costs still has 1,000,000 dollars available for settlement. Defense Outside Limits is more expensive but provides materially more protection on complex cases. On complex matters, the inside-vs-outside structure can be the difference between preserving indemnity for settlement and watching the limit erode during defense. The McDade Review checks the defense cost structure on every Professional Liability policy.

Who needs Professional Liability insurance in Texas?

Professional Liability insurance is relevant to any Texas business providing professional services, advice, or work product where a client could allege economic loss from the work. This includes IT services and software development firms, accountants and tax preparers, attorneys and legal practitioners, architects and engineers (often called design professional liability), real estate brokers and agents, financial advisors and investment professionals, healthcare practitioners (often called malpractice), marketing and advertising consultants, management and business consultants, insurance agents and brokers (carriers typically require E&O as a condition of appointment), home inspectors and property managers, education and training providers, and any other service-providing business where client decisions rely on your professional judgment. Many Texas commercial contracts now require Professional Liability as a contract condition, particularly in technology, design, and financial services.

How does Texas Insurance Code interact with Professional Liability claims?

Texas Insurance Code Chapter 38 (Unfair Settlement Practices) and Chapter 542 (Prompt Payment of Claims) impose statutory duties on Texas carriers handling professional liability claims, including statutory windows for claim acknowledgment and coverage decision, and additional damages for prompt-payment violations. The Texas Stowers Doctrine (Stowers Furniture Company v. American Indemnity Company, 1929) requires liability insurers to settle within policy limits when a reasonable insurer would do so, exposing carriers to liability beyond policy limits when the duty is breached. Texas Deceptive Trade Practices Act (DTPA) overlap creates a parallel cause of action on some Professional Liability claims, with treble damages available on some DTPA violations. The 2009 DTPA amendments narrowed coverage in some categories. The McDade Review evaluates the carrier's Texas claims-handling track record and the policy language against current Texas case law.

What is the McDade Professional Liability Review?

The McDade Professional Liability Review is an audit of your existing E&O policy by Dallas Downey, CLCS, with the McDade commercial team. The review evaluates four primary areas. First, the claims-made trigger and the Retroactive Date on the current policy, checking whether prior acts coverage is preserved and whether the Retroactive Date moved forward during any prior carrier change. Second, the Tail Coverage need at policy end and the cost ratio across carriers. Third, the defense cost structure (inside vs outside limits) against your operational exposure and claim severity profile. Fourth, exclusion language specific to your profession including the regulatory exclusion, the prior knowledge exclusion, the contractual liability exclusion, and any profession-specific exclusions. About 40 percent of the time the review confirms the current carrier and policy structure are correct. The other 60 percent identifies retroactive date exposures, defense cost gaps, or exclusion language opportunities.

Who handles Professional Liability at McDade?

Dallas Downey, CLCS leads the McDade commercial insurance team including Professional Liability. Dallas holds the Certified Lines Coverage Specialist designation and routes commercial conversations through a dedicated commercial meeting calendar. The McDade office serves the Houston metropolitan area including Spring, Klein, Tomball, Cypress, The Woodlands, Conroe, Humble, Katy, and Bridgeland, plus all of Texas through Premier Group Insurance carrier access including 50+ top Texas carriers we know well. McDade Insurance Brokerage Group is licensed by the Texas Department of Insurance (Texas License 2539471). Schedule a commercial review with Dallas through the commercial routing on this page or call the McDade office at 281.378.5002.

What Texas business owners say.

Real Google reviews from the Texas firms, professionals, and businesses the McDade team serves across Houston and the wider metro.

Send your current E&O declarations. Dallas Downey audits all three.

The McDade Professional Liability Review evaluates the claims-made trigger and retroactive date on your current policy, the tail coverage need and cost ratio across carriers, the defense cost structure (inside vs outside limits) against your operational exposure and claim severity profile, and the profession-specific exclusion language. Dallas Downey, CLCS leads the review. Most reviews complete inside one business week. About 40 percent of the time the audit confirms the current carrier and structure are correct. The other 60 percent identifies retroactive date exposures, defense cost gaps, or exclusion language opportunities.

Back to the commercial hub. Houston Business Insurance

Or call 281.378.5002

The review is advisory. McDade is licensed by the Texas Department of Insurance (Texas License 2539471).