Texas Workers Compensation Insurance

Your workers are covered. The class code decides what you pay.

Class codes, the experience modifier, and the annual payroll audit decide what workers compensation costs. We read all of it with you before the audit closes, not after.

Texas Workers Compensation, The McDade Way

Workers compensation is the one coverage Texas leaves optional, and the one where the price is set by details most employers never check. The class codes, the experience modifier, and the payroll audit. We translate the contract before claim time, so the premium you pay matches the work you actually do.

Six things worth reading line by line.

Medical Benefits

All reasonable and necessary medical care for the work-related injury, including hospital, prescription, physical therapy, and ongoing care. Texas Workers' Compensation Health Care Networks (WCHCN) control provider selection and rates if the employer participates.

Income Benefits

Temporary income benefits (TIBs) typically 70 percent of average weekly wage up to statutory caps. Impairment income benefits (IIBs), supplemental income benefits (SIBs), and lifetime income benefits (LIBs) for serious permanent injury per Texas Labor Code Section 408.

Death Benefits

Burial benefits and survivor income benefits for spouses, dependent children, and dependent parents of an employee killed on the job. Statutory amounts and eligibility per Texas Labor Code.

Employer's Liability (Part Two)

Defends and indemnifies the employer for employee injury suits not covered by workers comp benefits, including third-party-over actions, consequential injury suits by family members, and dual-capacity suits. Typically 500,000 to 1,000,000 dollars limit.

Tort Immunity (Subscribers Only)

A Texas employer that subscribes to workers compensation is statutorily immune from employee negligence suits arising from on-the-job injuries. Non-subscribers lose this immunity and face full civil court exposure including gross negligence and punitive damages.

Audit-Time Premium Reconciliation

Premium is initially estimated. At year-end audit, actual payroll across each class code is reconciled to true premium. Misclassification and arithmetic errors at audit are the most common Texas workers comp overpayment sources.

Texas WC is its own framework. The rules from other states do not apply here.

Texas workers compensation operates under the Texas Labor Code and is regulated by the Texas Department of Insurance Division of Workers' Compensation (DWC). The Texas system has several features that distinguish it from workers comp in other states.

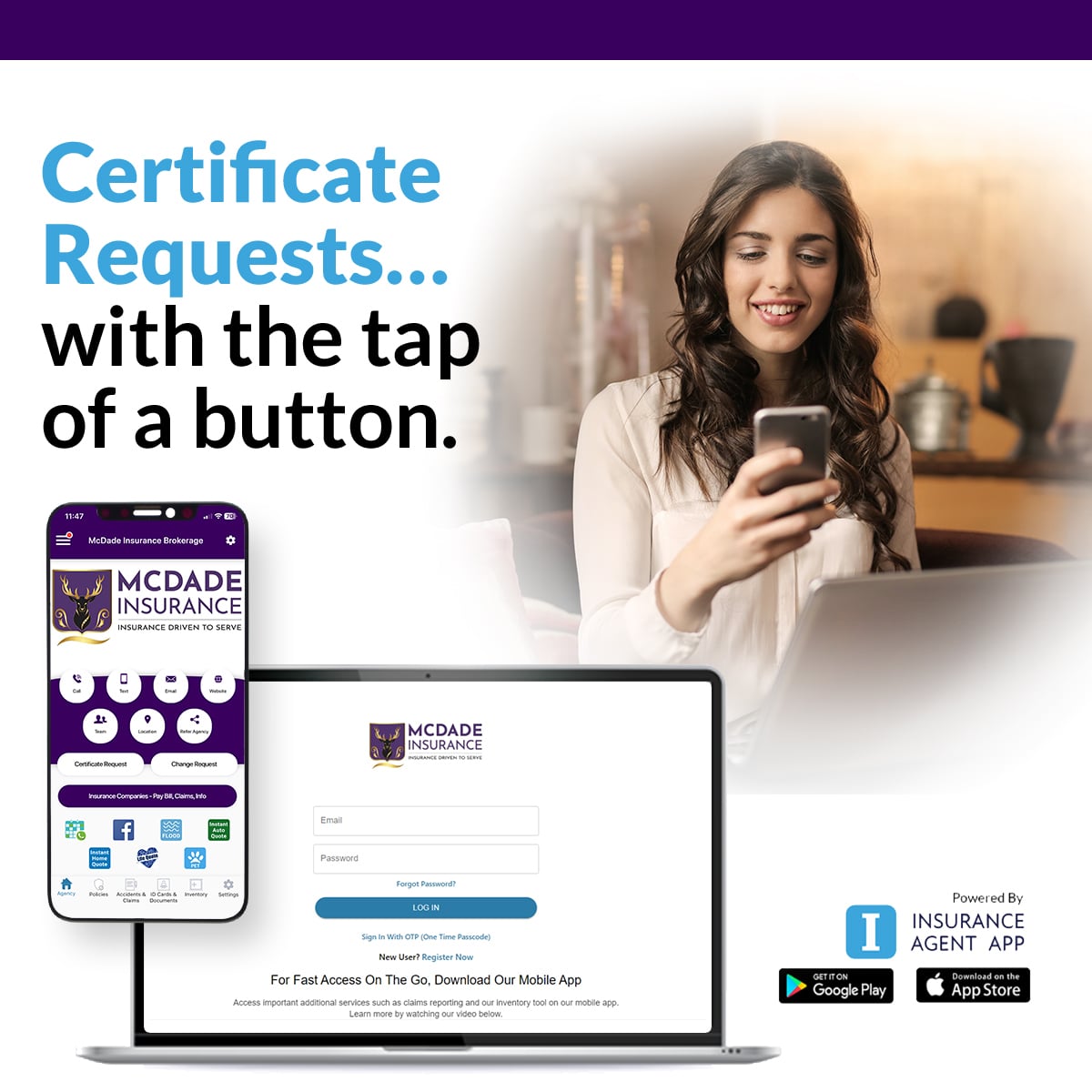

Your COIs. On Your Phone.

McDade clients get instant access to certificates of insurance from a mobile app. Issue. Email. Manage. No phone tag. No waiting on email.

Issue COIs on demand from your phone, anywhere, 24/7.

Email certificates directly to general contractors, vendors, or job sites in seconds.

Manage active certificates and policy info in one place.

Issue Certificates from your phone. The agency stays at the center.

If your business gets a certificate of insurance request twice a week, the McDade Client App removes that bottleneck. Pull an active certificate, edit the certificate holder, and email the COI to a general contractor, vendor, or job site directly from your phone in seconds. The app also handles auto ID cards, mobile claims documentation (especially relevant for workers comp incident documentation at the scene), asset inventory, and direct McDade team contact. Free to McDade clients. SOC 2 Type II compliant.

Certificates on Demand

Issue COIs showing workers comp coverage to general contractors in seconds.

Mobile Incident Documentation

Document workplace injuries from the scene with photos, witness notes, and GPS.

Auto ID Cards

Current commercial auto ID cards on field employees' phones for any DOT stop.

Direct McDade Contact

Tap to call Dallas Downey or the McDade service team about any open claim.

Built on the Insurance Agent App platform by GoInsuranceAgent, a Vertafore Orange Partner.

SOC 2 Type II compliantWorkers comp sits in a portfolio. Here is what sits next to it.

General Liability

Third-party bodily injury and property damage caused by your business operations. Most general contractors require both workers comp and general liability on every subcontractor certificate.

Commercial Auto

Commercial vehicles used in your business. Employees driving on the job carry exposure under both auto and workers comp. The hired and non-owned auto endorsement is critical for businesses with employees driving personal vehicles for work.

Commercial Property

Buildings, equipment, inventory, and business personal property. Property losses can produce business interruption that interacts with workers comp claim activity and payroll fluctuation.

Business Owners Policy (BOP)

A packaged commercial policy bundling general liability, commercial property, and often business income for small and mid-size businesses. Workers comp is sold separately. Most Texas BOPs target businesses that still fit the carrier's packaged-policy box.

Texas Workers Compensation. Read the questions worth asking.

Is workers compensation insurance required in Texas?

No. Texas is the only state in the United States where workers compensation insurance is optional for most private employers. Texas employers can choose to be subscribers (carrying workers comp) or non-subscribers (not carrying workers comp). The decision is strategic and carries significant trade-offs. Non-subscribers lose statutory immunity from employee lawsuits and can be sued in civil court for negligence following an on-the-job injury. Subscribers carry the workers comp policy that pays statutory medical and indemnity benefits in exchange for that immunity. The Texas Department of Insurance regulates workers compensation carriers in Texas through the Division of Workers' Compensation (DWC). Construction contracts and many large commercial contracts require workers comp from subcontractors regardless of the Texas optionality.

What is the Experience Modifier (X-Mod) and why does it matter?

The Experience Modifier, also called the X-Mod, EMR, or Mod, is a numerical multiplier calculated annually by NCCI (the National Council on Compensation Insurance) based on your business's loss history compared to the industry average for your class codes. An X-Mod of 1.00 is industry average. An X-Mod of 1.25 means your premium is multiplied by 1.25, costing you 25 percent more than an average employer in your class. An X-Mod of 0.85 means your premium is multiplied by 0.85, saving you 15 percent. The X-Mod is reported on the Unit Statistical Report each year. Errors are common, including misclassified claims, claims that should have been challenged, and data entry mistakes. Most Texas employers never audit their X-Mod, and the inflated X-Mod follows them for three policy years.

What is a class code and how is it determined?

NCCI assigns four-digit class codes to each occupation and job function within an employer's operations. Each class code carries its own base rate. Common Texas class codes include 8810 Clerical Office Employees, 8742 Outside Salespersons, 5403 Carpentry, 5645 Carpentry for Detached One or Two Family Dwellings, 5474 Painting NOC, 5022 Masonry NOC, and 9015 Building Operators. The class code assignment is based on the actual work performed, not the job title. Misclassification is one of the most common Texas workers comp audit errors. An office worker incorrectly classified as a construction laborer carries a premium multiple times higher than the correct rate. A class code audit identifies these errors and is the first step in the McDade Workers Compensation Review.

What happens at the annual workers compensation audit?

Workers compensation premium is initially estimated based on projected payroll at the start of the policy year. At the end of the policy year, the carrier audits actual payroll across each class code and reconciles the premium. If actual payroll exceeded the estimate, the employer owes additional premium. If actual payroll fell below the estimate, the employer receives a refund or credit. The audit is conducted by the carrier's auditor (in-person, telephone, or self-audit forms depending on premium size). Most Texas employers overpay at audit time due to misclassification of payroll (assigning higher-rate class codes to lower-rate work), inclusion of excluded compensation (overtime premium, severance, third-party sick pay), and arithmetic errors. McDade reviews the audit before the auditor finalizes and identifies dispute points.

What is a non-subscriber and what are the risks?

A Texas non-subscriber is a Texas employer that has elected to not carry workers compensation insurance. Non-subscribers must file a DWC Form 005 with the Texas Department of Insurance Division of Workers' Compensation and post notices in the workplace. The trade-off is significant. Non-subscribers lose statutory tort immunity, meaning an injured employee can sue the employer in civil court for negligence, gross negligence, and even punitive damages. Defenses like contributory negligence, assumption of risk, and fellow-servant rule are statutorily eliminated for non-subscribers in personal injury suits by employees. Many Texas non-subscribers carry an ERISA-style occupational accident plan to provide medical benefits without the workers comp framework. The Texas Department of Insurance specifically warns that non-subscriber status requires legal counsel review.

Can my Texas business use a Workers' Compensation Health Care Network?

Yes. Texas Labor Code Section 1305 allows certified Workers' Compensation Health Care Networks (WCHCN). Employers who notify employees in writing that they have established or joined a certified network direct injured employees to network providers for medical care. The network controls medical costs by negotiating provider rates and managing utilization. WCHCN participation typically produces material medical cost reduction over the life of the policy and can lower the workers comp premium through better claim experience. The Texas Department of Insurance maintains a list of certified Texas WCHCNs. Joining a network requires written employee notification with specific statutory language.

What credits and discounts are available on Texas workers compensation?

Texas workers compensation carriers offer multiple credits including drug-free workplace credits (typically 5 percent for documented drug-free workplace programs meeting Texas Labor Code requirements), return-to-work program credits (for documented light-duty and modified-duty programs), safety program credits, and employer-managed care or WCHCN participation credits. The Texas mandatory state-fund carrier Texas Mutual Insurance Company offers additional credits and a dividend program for policyholders. Pay-as-you-go workers comp (where premium is calculated and paid based on actual payroll through payroll system integration) can also smooth cash flow and reduce audit-time true-up exposure. The McDade Workers Compensation Review evaluates which credits the policy currently captures and which credits the employer is eligible for but not receiving.

How is workers compensation premium calculated?

Premium starts with the class code rate per 100 dollars of payroll, multiplied by the actual payroll within that class code, then multiplied by the Experience Modifier, then adjusted by schedule rating credits and debits (carrier underwriter discretion), then any applicable program credits (drug-free workplace, return-to-work, WCHCN), then expense constants and the Texas Department of Insurance assessments. The calculation produces the manual premium, the modified premium, and finally the deposit premium. Misclassification at the class code level, an inflated X-Mod, or missed credits each compounds through the calculation. A 20 percent X-Mod error on a 100,000-dollar payroll position can produce a 4,000 to 8,000 dollar annual overpayment that the employer never sees on a clearly labeled line item.

What is the McDade Workers Compensation Review?

The McDade Workers Compensation Review is an audit of the policyholder's existing workers compensation policy by Dallas Downey, CLCS, leading the McDade commercial team. The review evaluates three primary areas. First, the Experience Modifier (X-Mod) on the current Unit Statistical Report, with specific attention to misclassified claims, claims that should have been challenged, and data errors that inflated the Mod. Second, the class code assignments across the employer's payroll, with specific attention to misclassification (office work charged at construction rates, supervisory work charged at field rates, dual-occupation employees charged at the higher rate when they should be split). Third, the audit-time payroll reconciliation, with specific attention to excluded compensation (overtime premium, severance, third-party sick pay) and arithmetic errors. About 40 percent of the time the review confirms the current carrier and policy structure are correct. The other 60 percent identifies recoverable overpayments, X-Mod appeal grounds, or carrier and class code restructuring opportunities.

Who handles workers compensation at McDade?

Dallas Downey, CLCS leads the McDade commercial insurance team including workers compensation. Dallas holds the Certified Lines Coverage Specialist designation and routes workers compensation conversations through a dedicated workers compensation meeting calendar separate from general commercial intake. The McDade office serves the Houston metropolitan area including Spring, Klein, Tomball, Cypress, The Woodlands, Conroe, Humble, Katy, and Bridgeland, plus all of Texas through Premier Group Insurance carrier access. McDade Insurance Brokerage Group is licensed by the Texas Department of Insurance (Texas License 2539471). Schedule a workers compensation meeting with Dallas through the workers-comp routing on this page or call the McDade office at 281.378.5002.

What Texas business owners say.

Real Google reviews from the Texas employers, contractors, and businesses the McDade team serves across Houston and the wider metro.

Send your current WC policy. Dallas Downey audits all three.

The McDade Workers Compensation Review evaluates the Experience Modifier on your current Unit Statistical Report, the class code assignments across your payroll, and the audit-time payroll reconciliation from your last carrier audit. Dallas Downey, CLCS leads the review. Most reviews complete inside one business week. About 40 percent of the time the audit confirms the current carrier and structure are correct. The other 60 percent identifies recoverable overpayments or restructuring opportunities.

Back to the commercial hub. Houston Business Insurance

Or call 281.378.5002

The review is advisory. McDade is licensed by the Texas Department of Insurance (Texas License 2539471).