Houston General Liability Insurance

Your contract says you are covered. The endorsement decides if you are.

Additional insured forms, contract indemnity language, exclusions, and limits decide what a liability claim pays. We read all of it with you before a claim, not after.

General Liability, The McDade Way

The terms that decide a liability claim are written into your contracts and endorsements long before anything goes wrong. The additional insured form, the indemnity language, the exclusions, and the limits. We translate the contract before claim time, so the coverage you signed for is the coverage you actually have.

What General Liability Actually Covers. Six things worth reading line by line.

Coverage A: Bodily Injury and Property Damage

Third-party bodily injury and property damage arising from your operations, premises, or completed operations. Defense costs typically paid outside the per-occurrence limit. Per-occurrence and general aggregate limits structure the available coverage across the policy year.

Coverage B: Personal and Advertising Injury

Libel, slander, malicious prosecution, wrongful eviction, copyright or slogan infringement in your advertising. A separate per-offense limit applies. Common claim source for businesses with active marketing or content programs.

Coverage C: Medical Payments

Minor injury medical bills for non-employees injured on your premises, paid without regard to fault, typically up to 5,000 dollars per person. Streamlines small slip-and-fall claims and prevents minor incidents from escalating to litigation.

Additional Insured Endorsements

Extends coverage to general contractors, landlords, project owners, and other parties your contracts require. CG 20 10 covers ongoing operations only. CG 20 37 covers products-completed operations. CG 20 38 covers blanket additional insured by written contract. Form variant matters when the contract is signed years before the claim.

Defense Outside Limits

Defense costs are typically paid in addition to the per-occurrence limit (not eroding the limit). This is a core CGL distinction from claims-made policies. The defense obligation continues until the policy is exhausted by judgments or settlements.

Common Exclusions

Pollution, mold, asbestos, professional liability (E&O), employer's liability and workers compensation, auto liability, expected or intended injury, contractual liability except insured contracts, and damage to your own work or product. Coverage gaps in these exclusions are typically filled by separate policies.

Texas General Liability is its own framework. The rules from other states do not apply here.

Texas General Liability operates under the Texas Insurance Code and is shaped by Texas-specific case law on contractual indemnity, additional insured interpretation, and pollution exclusion limits. The Texas Department of Insurance regulates commercial liability carriers.

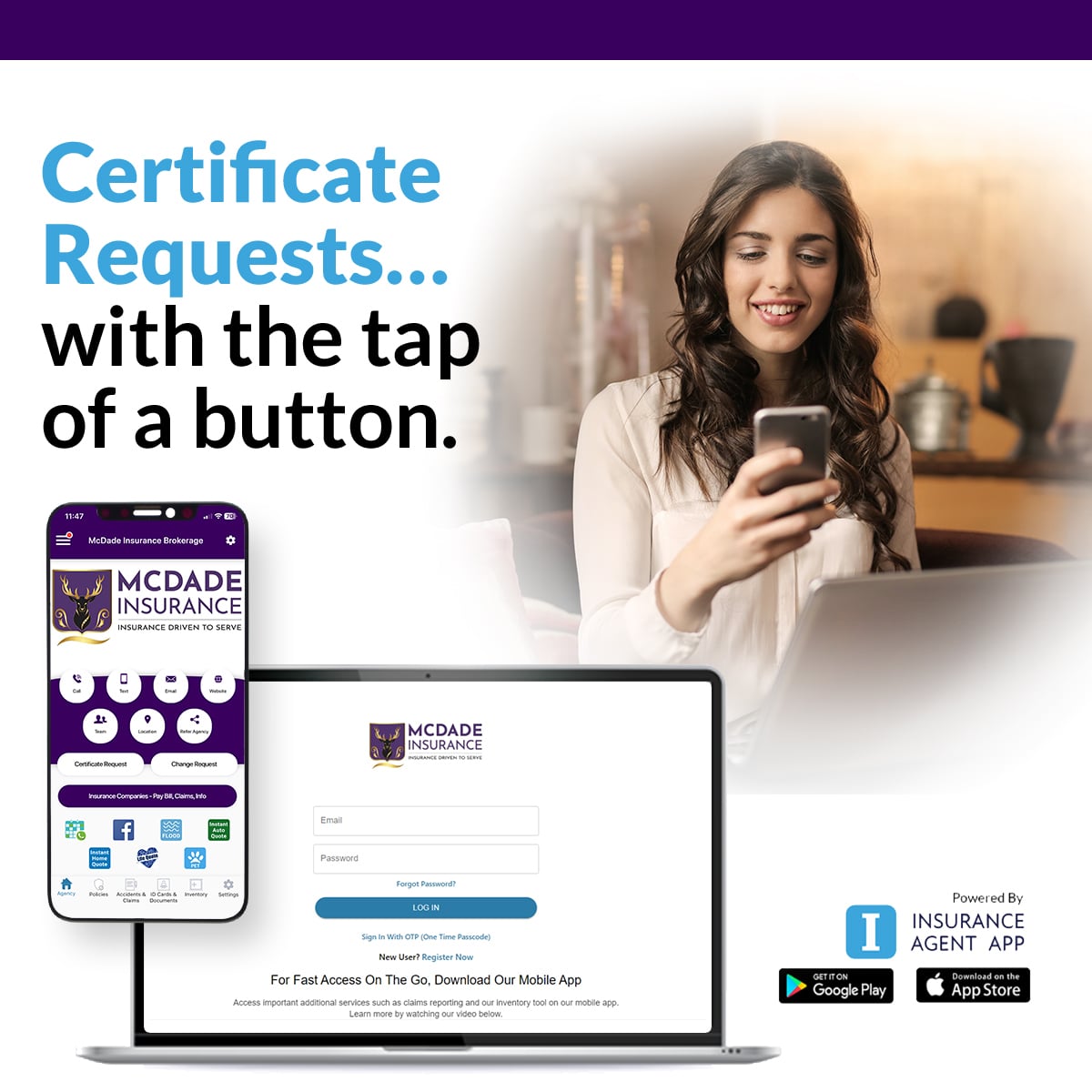

Your COIs. On Your Phone.

McDade clients get instant access to certificates of insurance from a mobile app. Issue. Email. Manage. No phone tag. No waiting on email.

Issue COIs on demand from your phone, anywhere, 24/7.

Email certificates directly to general contractors, vendors, or job sites in seconds.

Manage active certificates and policy info in one place.

Issue Certificates from your phone. The agency stays at the center.

If your business gets a certificate of insurance request twice a week, the McDade Client App removes that bottleneck. Pull an active certificate, edit the certificate holder, and email the COI to a general contractor, vendor, or job site directly from your phone in seconds. The app also handles auto ID cards, mobile claims documentation, asset inventory, and direct McDade team contact. Free to McDade clients. SOC 2 Type II compliant.

Certificates on Demand

Issue COIs and email directly to general contractors in seconds.

Auto ID Cards

Current Texas auto ID cards on your phone for traffic stops and rentals.

Mobile Claims Kit

Document accidents and losses from the scene with photos and notes.

Asset Inventory

Maintain documented inventory of business equipment for claim time.

Built on the Insurance Agent App platform by GoInsuranceAgent, a Vertafore Orange Partner.

SOC 2 Type II compliantThis coverage sits in a portfolio. Here is what sits next to it.

Commercial Property

Buildings, equipment, inventory. The natural companion coverage to GL. Most Texas commercial policies bundle the two as a Business Owners Policy or as separate policies on a single program.

Commercial Auto

Auto liability for company vehicles, plus the critical Hired and Non-Owned Auto endorsement for employees driving personal vehicles for work.

Texas Workers Compensation

Statutory benefits for employees injured on the job. Texas WC is optional but creates a separate exposure layer interacting with GL Employer's Liability exclusion.

Business Owners Policy (BOP)

Packaged general liability + commercial property + business income for small and mid-size Texas businesses. Most TX BOPs target businesses with under 500 employees.

General Liability Insurance. Read the questions worth asking.

What is General Liability Insurance and what does it cover?

General Liability Insurance is the foundation commercial liability coverage that protects your business against third-party bodily injury, property damage, personal and advertising injury, and limited medical payments arising from your operations, premises, or completed operations. The Insurance Services Office standard form is the Commercial General Liability form CG 00 01. Coverage A covers bodily injury and property damage. Coverage B covers personal and advertising injury. Coverage C covers medical payments. Defense costs are typically paid in addition to the limit. The policy is occurrence-based, meaning the policy in force when the injury or damage occurs responds regardless of when the claim is reported.

What is an Additional Insured endorsement and why does the form variant matter?

An Additional Insured endorsement extends General Liability coverage to a third party (typically a general contractor, landlord, or project owner) that your contract requires you to cover. The form variant on the endorsement decides what scope of coverage applies. CG 20 10 covers the additional insured for ongoing operations only. CG 20 37 covers products and completed operations (claims reported after the work is finished). CG 20 38 (2013 ISO blanket version) covers any party required by written contract. Older blanket forms have narrower coverage. Most Texas construction and lease disputes turn on which form variant is in the policy, not whether an endorsement exists.

What is the Texas Anti-Indemnity Act and how does it interact with my CGL?

Texas Insurance Code Chapter 151 is the Texas Anti-Indemnity Act. The statute limits broad-form indemnification in construction contracts. A construction contract cannot require an indemnitor to defend or indemnify another party for that party's own negligence in most circumstances. The interaction with CGL is significant. An Additional Insured endorsement that would otherwise extend coverage to a general contractor for the contractor's own negligence may be limited by Chapter 151. The McDade General Liability Review evaluates the contract indemnity language alongside the CGL Additional Insured endorsement to identify whether the coverage you assumed exists actually exists under Texas law.

How do per-occurrence and general aggregate limits work?

A General Liability policy typically has a per-occurrence limit (the maximum the policy pays for any one claim) and a general aggregate limit (the maximum the policy pays across all claims during the policy year). A 1,000,000 dollar per-occurrence and 2,000,000 dollar general aggregate policy can pay 1,000,000 dollars for any single claim and up to 2,000,000 dollars total across the year. Products-completed operations typically has a separate aggregate limit. Personal and advertising injury has a separate limit per offense. The McDade Review evaluates whether the limit structure matches your operational exposure and contract requirements.

What is the Stowers Doctrine and why does it matter for Texas businesses?

The Stowers Doctrine comes from the 1929 Texas Supreme Court decision in Stowers Furniture Company v. American Indemnity Company. The doctrine requires liability insurers to settle within policy limits when a reasonable insurer would do so. If the carrier refuses to settle within limits and the case ultimately produces a judgment above limits, the carrier can be liable for the full judgment beyond the policy limits. The Stowers demand is a standard Texas pre-trial document that triggers the carrier's duty. The doctrine protects insureds from carrier overconfidence at trial. Texas commercial carriers structure their claims practices around Stowers.

What does General Liability NOT cover?

Common CGL exclusions include pollution, mold, asbestos, professional liability (Errors and Omissions), employer's liability and workers compensation (covered by WC policy), auto liability (covered by Commercial Auto), expected or intended injury, contractual liability except for insured contracts, damage to your own work or product, liquor liability for businesses serving alcohol, communicable disease (added broadly post-2020), and electronic data and cyber exposures (covered by Cyber Liability policies). Most Texas businesses fill these exclusion gaps with separate policies.

How are General Liability premiums calculated for Texas businesses?

GL premium starts with the carrier's class code rate per 1,000 dollars of exposure base (which is typically annual revenue, payroll, or square footage depending on the business class). The premium is multiplied by the carrier's schedule rating modifier (carrier underwriter discretion for risk quality), then adjusted by experience rating where applicable, then any program credits (loss control program, safety committee, contractor licensing). Construction-related GL is typically rated on payroll because payroll correlates with operations exposure. Retail and office GL is typically rated on annual revenue or square footage. Misclassification at the class code level produces the most common Texas GL overpayment.

What is the McDade General Liability Review?

The McDade General Liability Review is an audit of the policyholder's existing GL policy by Dallas Downey, CLCS. The review evaluates three primary areas. First, the Additional Insured endorsement form variants on the current policy, with specific attention to whether the form matches what your contracts actually require. Second, the indemnity provisions in your active contracts against the Texas Anti-Indemnity Act (Chapter 151), identifying provisions that may be unenforceable or that create unfunded risk. Third, the limit structure (per-occurrence, general aggregate, products-completed operations aggregate, personal injury per offense) against your operational exposure. About 40 percent of the time the review confirms the current carrier and policy structure are correct. The other 60 percent identifies endorsement gaps, contract language exposures, or carrier restructuring opportunities.

Does my General Liability policy cover claims by my own employees?

No. Claims by your own employees for on-the-job injuries are excluded from General Liability and are the function of Workers Compensation. The Employer's Liability exclusion on the CGL form is explicit. If you are a Texas subscriber to Workers Compensation, your WC policy responds to employee injury claims. If you are a Texas non-subscriber (the optional path Texas allows), you face civil court exposure for employee injury claims that your GL does not cover. The McDade team coordinates Workers Compensation and General Liability programs because the two policies sit next to each other in the same commercial program.

Who handles General Liability at McDade?

Dallas Downey, CLCS leads the McDade commercial insurance team including General Liability. Dallas holds the Certified Lines Coverage Specialist designation and routes commercial conversations through a dedicated commercial meeting calendar. The McDade office serves the Houston metropolitan area including Spring, Klein, Tomball, Cypress, The Woodlands, Conroe, Humble, Katy, and Bridgeland, plus all of Texas through Premier Group Insurance carrier access including 50+ top Texas carriers we know well. McDade Insurance Brokerage Group is licensed by the Texas Department of Insurance (Texas License 2539471). Schedule a commercial review with Dallas through the commercial routing on this page or call the McDade office at 281.378.5002.

What Texas business owners say.

Real Google reviews from the Texas contractors, trades, and businesses the McDade team serves across Houston and the wider metro.

Send your current GL policy. Dallas Downey audits all three.

The McDade General Liability Review evaluates the Additional Insured endorsement form variants on your current policy, the indemnity provisions in your active contracts against the Texas Anti-Indemnity Act, and the limit structure against your operational exposure. Dallas Downey, CLCS leads the review. Most reviews complete inside one business week. About 40 percent of the time the audit confirms the current carrier and structure are correct. The other 60 percent identifies endorsement gaps, contract exposures, or restructuring opportunities.

Back to the commercial hub. Houston Business Insurance

Or call 281.378.5002

The review is advisory. McDade is licensed by the Texas Department of Insurance (Texas License 2539471).