Houston Commercial Property Insurance

Your building is covered. The contract decides how well.

Coinsurance, the Texas wind and hail percentage deductible, business income, and the roof endorsement decide what a property claim actually pays. We read all of it with you while you can still change it.

Commercial Property Insurance, The McDade Way

The terms that decide a Texas property claim are written long before the claim. Coinsurance, the wind and hail percentage deductible, the roof endorsement, and the business income limit. We translate the contract before claim time, so you know what every line means while you can still change it.

What Commercial Property Actually Covers. Six clauses worth reading at renewal time.

Buildings and Structures

The physical building, attached additions, permanent fixtures, and outdoor signs. Replacement Cost Value (RCV) endorsement is standard. Building ordinance and law endorsement covers code-upgrade costs at rebuild. Most Texas policies sub-limit specific items like signs and landscaping.

Business Personal Property

Equipment, machinery, inventory, furniture, fixtures, and other contents not permanently attached to the building. Includes property of others in your care, custody, or control up to a sub-limit. Off-premises coverage applies in transit and at temporary storage locations.

Business Income (Interruption)

Lost net profit plus continuing normal operating expenses during the period of restoration. Coverage typically begins 72 hours after the loss and continues until the property is restored or for a stated period of indemnity. The 12-month standard period of indemnity is the default. Extended Business Income covers continued reduced revenue after reopening.

Extra Expense

Reasonable costs to minimize the business income loss including temporary location rent, expedited shipping, temporary equipment rental, and overtime payroll. Paid in addition to Business Income. Extra Expense Only forms exist for businesses with no business income exposure but high continuity costs.

Ordinance or Law Coverage

Three coverages bundled. Coverage A pays the value of the undamaged portion of the building that must be demolished due to code. Coverage B pays the demolition cost. Coverage C pays the increased cost of construction to current code. Critical for older Texas buildings and any building near current code thresholds.

Equipment Breakdown

Mechanical and electrical breakdown of boilers, HVAC, refrigeration, electrical panels, production equipment, and computer systems. Standard Commercial Property forms typically exclude breakdown. Equipment Breakdown endorsement or stand-alone policy fills the gap. Critical for restaurants, manufacturers, and any business with capital-intensive equipment.

Texas commercial property is its own framework. Wind, hail, freeze, and coinsurance.

Texas commercial property operates under the Texas Insurance Code and is shaped by Texas-specific exposure including wind and hail (state-leading frequency and severity), freeze events (the 2021 winter storm Uri rewrote Texas policy language), and the percentage deductible structure that distinguishes Texas commercial property from many other states.

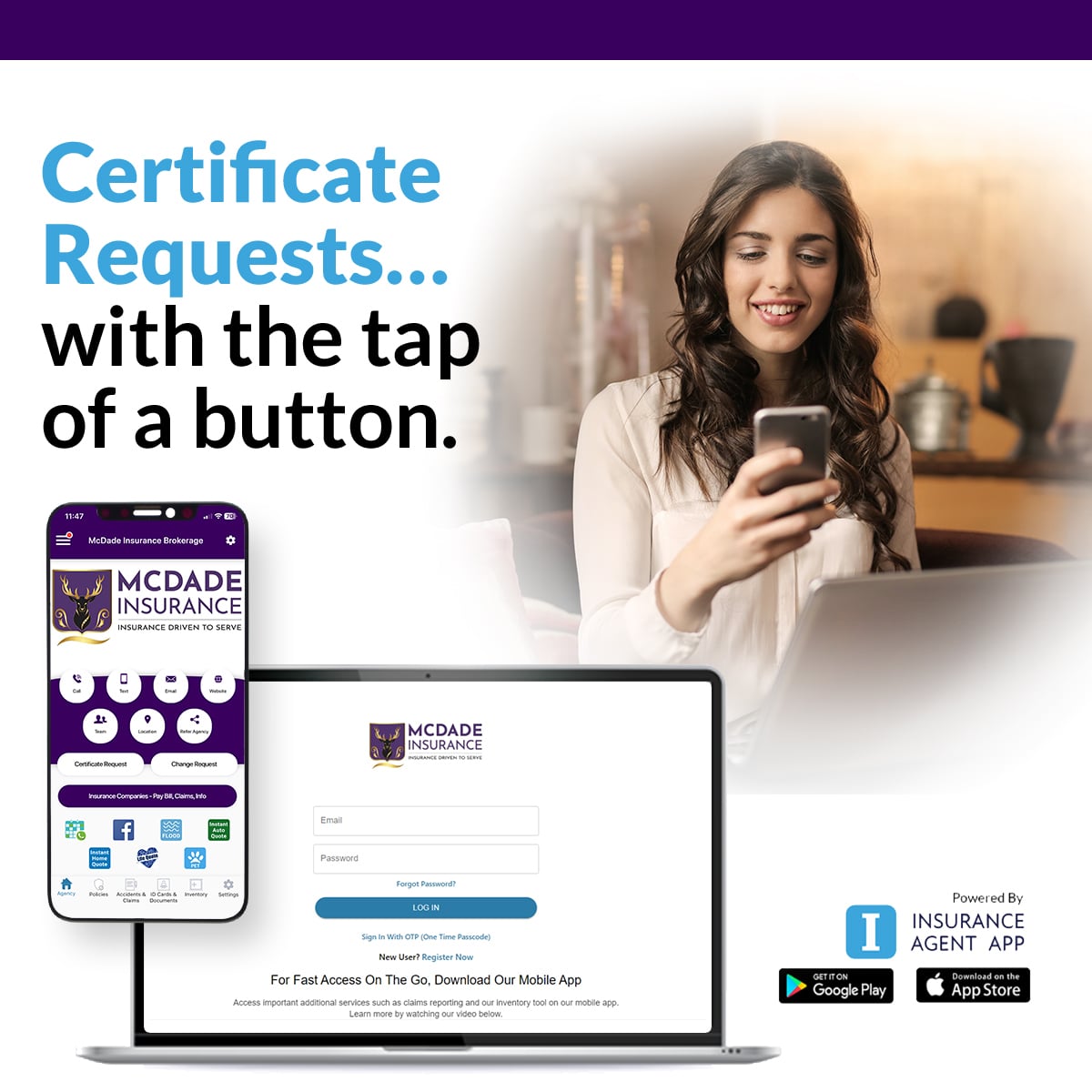

Your COIs. On Your Phone.

McDade clients get instant access to certificates of insurance from a mobile app. Issue. Email. Manage. No phone tag. No waiting on email.

Issue COIs on demand from your phone, anywhere, 24/7.

Email certificates directly to general contractors, vendors, or job sites in seconds.

Manage active certificates and policy info in one place.

Issue Certificates from your phone. The agency stays at the center.

If your business gets a certificate of insurance request twice a week, the McDade Client App removes that bottleneck. Pull an active certificate, edit the certificate holder, and email the COI to a general contractor, vendor, or job site directly from your phone in seconds. The app also handles auto ID cards, mobile claims documentation, asset inventory, and direct McDade team contact. Free to McDade clients. SOC 2 Type II compliant.

Certificates on Demand

Issue COIs and email directly to general contractors in seconds.

Auto ID Cards

Current Texas auto ID cards on your phone for traffic stops and rentals.

Mobile Claims Kit

Document accidents and losses from the scene with photos and notes.

Asset Inventory

Maintain documented inventory of business equipment for claim time.

Built on the Insurance Agent App platform by GoInsuranceAgent, a Vertafore Orange Partner.

SOC 2 Type II compliantThis coverage sits in a portfolio. Here is what sits next to it.

General Liability

Third-party bodily injury and property damage from your operations. The natural companion to commercial property. Most Texas businesses carry both in a coordinated program.

Business Owners Policy (BOP)

Packaged general liability + commercial property + business income for small and mid-size businesses. A BOP can be efficient when the business still fits the carrier's packaged-policy box.

Texas Builders Risk

Commercial property coverage during the construction phase of a project. Replaces standard property coverage from groundbreaking through completion and turnover.

Commercial Auto

Auto physical damage and liability for company-owned vehicles. Vehicles are not covered under commercial property policies and require a separate commercial auto program.

Commercial Property Insurance. Read the questions worth asking.

What does Commercial Property Insurance cover?

Commercial Property Insurance covers physical damage to your business buildings, equipment, inventory, and business personal property from covered perils, plus the income and extra expense you incur while the business cannot operate normally during the repair period. Standard Insurance Services Office forms include the Building and Personal Property Coverage Form (CP 00 10), Business Income Coverage Form (CP 00 30), and Causes of Loss Special Form (CP 10 30). Coverage applies on Replacement Cost Value (RCV) or Actual Cash Value (ACV) basis depending on the endorsement, and is subject to coinsurance, deductibles, and any specific perils excluded by the carrier.

What is the Texas Wind/Hail percentage deductible and why does it matter?

Most Texas commercial property policies apply a separate percentage deductible to wind and hail losses, typically 1 to 5 percent of the building value (not the loss amount). For example, a 1,000,000 dollar building with a 2 percent wind/hail deductible carries a 20,000 dollar out-of-pocket exposure on every wind or hail loss, regardless of how small the loss is. This is fundamentally different from a flat deductible policy in lower-hail states. The percentage applies per building per occurrence. The McDade Review evaluates whether the percentage matches your reserves and whether the carrier offers a lower percentage option.

What is coinsurance and how does the penalty work?

The coinsurance clause requires you to insure to a stated percentage (typically 80 or 90 percent) of the building's replacement cost at the time of loss. If actual insured value falls short of the required percentage when a loss occurs, the carrier reduces the claim payment proportionally by the underinsurance ratio. A building insured for 700,000 dollars when actual replacement cost is 1,000,000 dollars (and 80 percent coinsurance applies, so 800,000 dollars was required) receives 87.5 percent of any covered loss (700,000 divided by 800,000), not the policy limit. Coinsurance penalties become visible at claim time, not at renewal. McDade audits coinsurance compliance annually as part of the Commercial Property Review.

What is Replacement Cost Value vs Actual Cash Value?

Replacement Cost Value (RCV) pays the cost to replace damaged property with new property of like kind and quality, without deduction for depreciation. Actual Cash Value (ACV) pays RCV minus depreciation for age, wear, and obsolescence. RCV is the standard endorsement on most Texas commercial property policies for the building itself. ACV is common for personal property older than 10 years, for roofs older than 10 to 15 years, and in some carrier-specific endorsements after recent loss activity. A 15-year-old roof valued at 80,000 dollars new might receive 30,000 to 40,000 dollars under ACV. The roof endorsement on your current policy is one of the highest-impact line items in the entire Commercial Property contract.

How does Business Income coverage work?

Business Income coverage pays lost net profit plus continuing normal operating expenses during the period of restoration (the time required to repair or rebuild the damaged property and resume normal operations). Coverage typically begins 72 hours after the loss (the waiting period). The standard period of indemnity is 12 months. Extended Business Income covers continued reduced revenue after reopening, typically for 30 to 60 days. Calculation of the Business Income limit requires a 12-month projection of net profit plus continuing expenses, which most Texas businesses underestimate. The McDade Review evaluates the Business Income limit against current revenue and operating expense structure.

What is Equipment Breakdown coverage and do I need it?

Equipment Breakdown coverage pays for mechanical and electrical breakdown of boilers, HVAC systems, refrigeration, electrical panels, production equipment, and computer systems. Standard Commercial Property forms typically exclude breakdown (sudden mechanical or electrical failure not caused by an external peril). Equipment Breakdown endorsement (CP 10 50 or carrier proprietary forms) or a stand-alone policy fills the gap. Critical for restaurants (refrigeration), manufacturers (production equipment), property managers (HVAC and elevators), data-dependent businesses (servers and electrical), and any business with capital-intensive equipment. Most Texas Business Owners Policies include limited Equipment Breakdown automatically.

What is Ordinance or Law coverage and why is it important for Texas buildings?

Ordinance or Law coverage is three coverages bundled. Coverage A pays the value of the undamaged portion of the building that must be demolished due to building code requirements after a partial loss. Coverage B pays the demolition cost. Coverage C pays the increased cost of construction to current code. Critical for older Texas buildings (pre-2000 construction), buildings in flood-prone areas where code has changed, buildings in coastal Texas counties with updated windstorm code, and any building where current code requires upgrades the original construction did not include. Without Ordinance or Law, a 60-percent loss may force a full demolition with the un-rebuilt portion at the owner's expense.

How are Texas Wind and Hail losses adjusted differently from other property losses?

Texas wind and hail losses use a separate percentage deductible (typically 1 to 5 percent of building value) rather than a flat dollar deductible. The deductible applies per building per occurrence. Adjustment process is similar to other property losses but with two differences. First, hail-event scoping (counting impact damage versus pre-existing damage on roofs and siding) is contested in many Texas hail claims and uses standardized adjuster methodologies. Second, roof endorsement variants (ACV on roofs, schedule-rated depreciation, cosmetic exclusions) change the payable amount on roof claims. The McDade Review identifies the roof endorsement and the wind/hail deductible structure on your current policy.

What is the McDade Commercial Property Review?

The McDade Commercial Property Review is an audit of your existing commercial property policy by Dallas Downey, CLCS. The review evaluates three primary areas. First, the coinsurance compliance ratio against your current replacement cost values, identifying underinsurance exposure that would reduce claim payments. Second, the wind/hail percentage deductible and the roof endorsement variant against your building age, roof age, and Texas county location. Third, the Business Income limit, period of indemnity, and Extra Expense limit against your current 12-month revenue and operating expense projection. About 40 percent of the time the review confirms the current structure is correct. The other 60 percent identifies coinsurance gaps, deductible restructuring opportunities, or Business Income limit shortfalls.

Who handles Commercial Property at McDade?

Dallas Downey, CLCS leads the McDade commercial insurance team including Commercial Property. Dallas holds the Certified Lines Coverage Specialist designation and routes commercial conversations through a dedicated commercial meeting calendar. The McDade office serves the Houston metropolitan area including Spring, Klein, Tomball, Cypress, The Woodlands, Conroe, Humble, Katy, and Bridgeland, plus all of Texas through Premier Group Insurance carrier access including 50+ top Texas carriers we know well. McDade Insurance Brokerage Group is licensed by the Texas Department of Insurance (Texas License 2539471). Schedule a commercial review with Dallas through the commercial routing on this page or call the McDade office at 281.378.5002.

What Texas business owners say.

Real Google reviews from the Texas families and businesses McDade serves across Houston, Spring, and the wider metro.

Send your current property declarations. Dallas Downey audits all three.

The McDade Commercial Property Review evaluates the coinsurance compliance ratio against your current replacement cost values, the wind/hail percentage deductible and roof endorsement variant against your building age and Texas county, and the Business Income limit and period of indemnity against your current operating profile. Dallas Downey, CLCS leads the review. Most reviews complete inside one business week. About 40 percent of the time the audit confirms the current structure is correct. The other 60 percent identifies coinsurance gaps, deductible opportunities, or Business Income shortfalls.

Back to the commercial hub. Houston Business Insurance

Or call 281.378.5002

The review is advisory. McDade is licensed by the Texas Department of Insurance (Texas License 2539471).