A breach is not just an IT problem. It is a contract and recovery problem.

Cyber liability insurance has to respond to the real sequence after an event: breach response, business interruption, ransomware, privacy duties, social engineering, and client contract requirements. The McDade Cyber Liability Review reads the policy against how your business actually works. Dallas Downey, CLCS leads the commercial review, with Charles McDade's family background in Houston cybersecurity informing the lens.

First-party costs. Third-party liability. And what your business needs after the attack.

Cyber Liability Insurance covers the costs your business incurs after a cyber incident (first-party) and the liability your business faces from third parties harmed by the incident (third-party). First-party coverage typically includes incident response and forensic investigation, legal counsel during the incident, ransom payment subject to OFAC compliance and carrier consent, business interruption income loss during recovery, system restoration and data recovery, breach notification to affected individuals as required by Texas Business and Commerce Code Chapter 521, credit monitoring services, and public relations crisis response. Third-party coverage typically includes privacy liability for failure to protect personally identifiable information, network security liability for transmission of harmful code or denial-of-service conditions, regulatory defense and fines including Texas Data Privacy and Security Act actions, Payment Card Industry assessment defense, and media liability for online content. Optional endorsements add social engineering fraud, reputational harm, contingent business interruption for vendor outages, and cryptojacking. The Texas Data Privacy and Security Act (TDPSA) took effect July 1, 2024 and the cure period expired January 1, 2025. The Texas Attorney General has filed over 100 investigations and the first TDPSA lawsuit was filed January 13, 2025, against Allstate Corporation and Arity subsidiaries with the state claiming over 1,000,000 dollars in monetary relief. Dallas Downey, CLCS leads the McDade commercial team. Charles McDade reviews cyber policies alongside Dallas, drawing on the family background in endpoint security through Naknan Inc.

"The cyber lineage in my family runs to Houston, 1997. My grandfather, the late Douglas Finley, founded Naknan Inc., a Houston Clear Lake area endpoint security and IT services firm. Naknan operated in the NASA corridor for over two decades, building patch management, security software, and IT infrastructure for commercial and government clients. I grew up understanding that cybersecurity is not abstract. It is what working families build businesses around in Houston. The McDade Cyber Liability Review carries that family understanding into the broker's chair. Cyber liability insurance does not prevent the attack. Cyber liability insurance, paired with appropriate security controls, prevents the closure that follows the attack."

Charles McDade, LUTCF · Founder, McDade Insurance Brokerage Group · Grandson of the late Douglas Finley, founder of Naknan Inc.

Eight coverage lines. First-party and third-party, side by side.

First-Party: Incident Response and Forensics

Forensic investigation to determine what happened, how the attackers entered, what data was exposed, and what systems were affected. Legal counsel during the incident. Most incidents require both within 24 hours of discovery. Industry data shows median breach detection time of 181 days.

First-Party: Ransom and Cyber Extortion

Coverage for ransom payment subject to OFAC compliance and carrier consent. The U.S. Treasury OFAC restricts payments to sanctioned actors regardless of insurance. Research shows 69 percent of ransom-paying businesses were attacked again and 82 percent paid less than the original demand.

First-Party: Business Income Interruption

Lost net profit plus continuing normal operating expenses during system recovery. Recovery cost varies by outage length, systems affected, vendors, and whether data notification is required. Period of indemnity is the audit checkpoint.

First-Party: System Restoration and Data Recovery

Cost to restore systems, reinstall software, recover or reconstruct lost data, and rebuild compromised infrastructure. Includes hardware replacement when forensics requires it. Includes the costly process of rebuilding from backups that were also encrypted (an increasingly common pattern in 2025-2026 ransomware).

First-Party: Breach Notification and Credit Monitoring

Cost of identifying affected individuals, drafting and sending notification letters as required by Texas Business and Commerce Code Chapter 521, providing credit monitoring services to affected individuals typically for 12 months, and Texas Attorney General notification for breaches affecting 250 or more Texas residents.

Third-Party: Privacy Liability

Defense and indemnity for lawsuits alleging failure to protect personally identifiable information, protected health information, payment card data, biometric data, or other sensitive consumer or employee data. Includes class action defense, which is the most common Texas privacy lawsuit pattern.

Third-Party: Regulatory Defense and Fines

Defense costs and insurable fines from Texas Attorney General TDPSA actions, Federal Trade Commission actions, Department of Health and Human Services HIPAA actions, Payment Card Industry assessments, and Texas Identity Theft Enforcement and Protection Act enforcement. TDPSA penalties scale at 7,500 dollars per affected consumer.

Social Engineering Fraud

The fake CEO email, the fake vendor invoice, the voice-cloned phone call. Social engineering losses are commonly handled by endorsement and sub-limit. This is often the gap that looks small on the declarations page and large when the money leaves the account.

What actually happens. And why the policy has to fund recovery.

Discovery (typically 181 days after initial compromise)

Industry research shows the median time from initial system compromise to detection is 181 days. The attacker has been inside the network for roughly six months by the time anyone notices. Many SMB incidents are first detected by a third party, often a payment processor flagging fraudulent activity or a vendor noticing irregular communication.

Incident Response (0 to 72 hours)

Carrier-approved forensic team mobilizes. Legal counsel engages. Systems get isolated. Decisions about ransom payment, OFAC compliance, and law enforcement notification get made under pressure. Cyber liability policies pay for the incident response panel of carrier-approved vendors. Businesses without coverage pay these costs out of operating capital at retail rates.

Business Interruption (typically 14 to 30 days for ransomware)

Systems are offline. Revenue stops. Customers cannot reach you. Continuing expenses continue. This is where the business interruption period, waiting period, and period of indemnity become more than insurance words; they decide whether the policy can help fund the recovery window.

Breach Notification (typically within 60 days, Chapter 521 deadline)

Texas Business and Commerce Code Chapter 521 requires notification to affected Texas residents as quickly as possible, generally within 60 days of breach discovery. Texas Attorney General notification is required for breaches affecting 250 or more Texas residents. Credit monitoring for affected individuals typically runs 12 months. This step has fixed regulatory deadlines and triggers customer churn.

Customer Churn and Contract Cancellations (90 to 180 days)

Once breach notification goes out, customer attrition begins. B2B customers with security clauses in their vendor contracts often have automatic termination rights triggered by a breach notification. Texas businesses serving healthcare facilities, financial institutions, and large general contractors frequently lose 20 to 50 percent of contracted revenue in the 6 months following a notified breach. This is the phase where most uninsured small businesses close.

Regulatory Defense and Civil Litigation (6 to 36 months)

Regulatory questions, consumer complaints, payment-card assessments, vendor disputes, and contract claims may arrive after operations come back online. Third-party liability coverage, privacy defense, PCI coverage, and regulatory defense sub-limits decide how much help the policy provides in that second wave.

The Texas regulatory map for cyber is newer and tighter. And the Attorney General has filed the first lawsuits.

Texas cyber compliance changed materially on July 1, 2024 when the Texas Data Privacy and Security Act took effect. The 30-day cure period expired January 1, 2025, which means the Attorney General can now proceed directly to civil enforcement without a remediation window. The first TDPSA lawsuit was filed on January 13, 2025, against Allstate Corporation and five Arity subsidiaries, with the state claiming over 1,000,000 dollars in monetary relief.

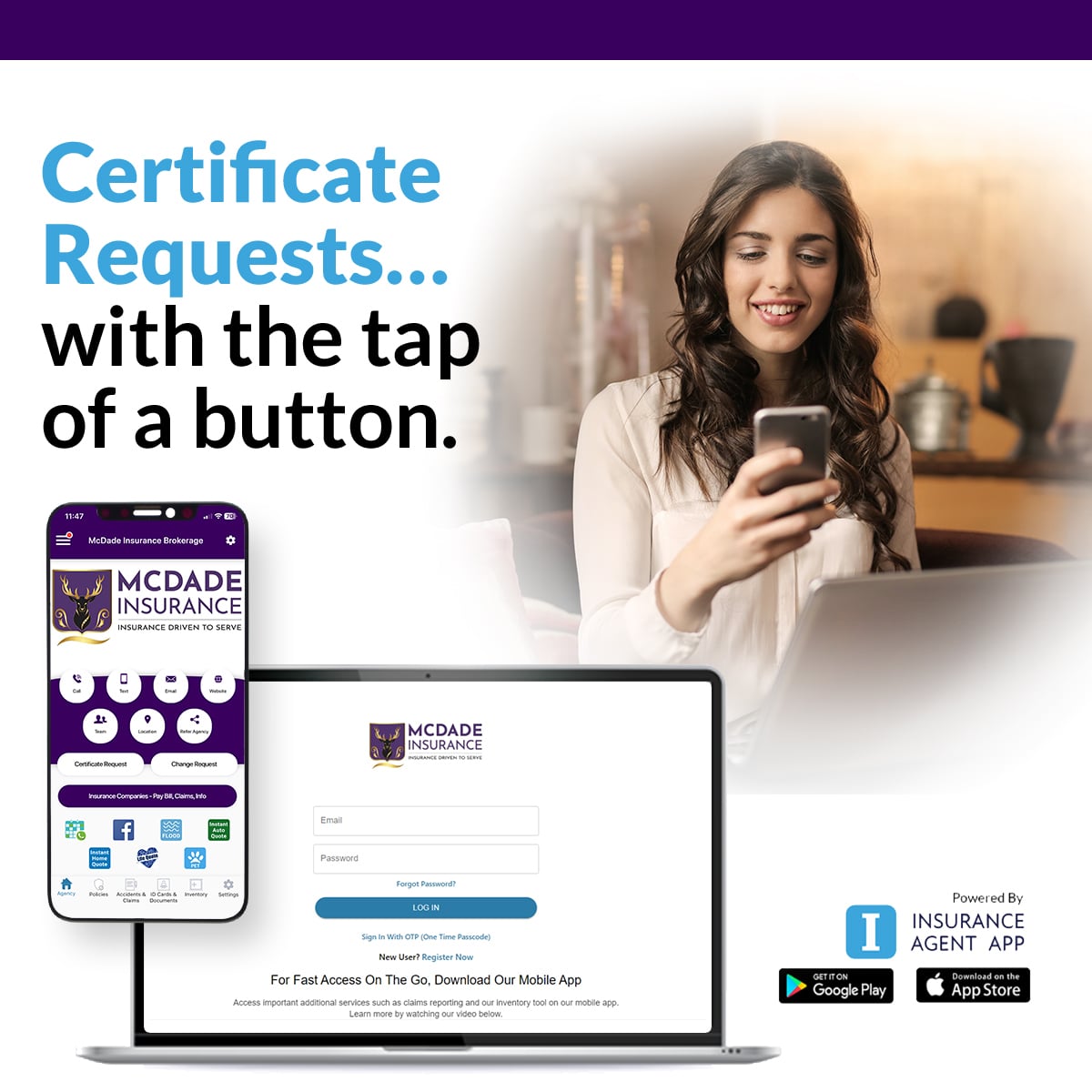

Your COIs. On Your Phone.

McDade clients get instant access to certificates of insurance from a mobile app. Issue. Email. Manage. No phone tag. No waiting on email.

Issue COIs on demand from your phone, anywhere, 24/7.

Email certificates directly to general contractors, vendors, or job sites in seconds.

Manage active certificates and policy info in one place.

Issue Certificates from your phone. The agency stays at the center.

If your business gets a certificate of insurance request twice a week, the McDade Client App removes that bottleneck. Pull an active certificate, edit the certificate holder, and email the COI to a general contractor, vendor, or job site directly from your phone in seconds. Cyber liability coverage on COIs is increasingly required by Texas healthcare facilities, financial institutions, and large general contractors. The app also handles auto ID cards, mobile claims documentation, asset inventory, and direct McDade team contact. Free to McDade clients. SOC 2 Type II compliant.

Certificates on Demand

Issue COIs showing cyber and commercial coverage to clients in seconds.

Incident Documentation

Document the timeline of a cyber incident with timestamps and uploaded artifacts.

Auto ID Cards

Current commercial auto ID cards on employee phones for any DOT or traffic stop.

Direct McDade Contact

Tap to call Dallas Downey or Charles McDade about any open cyber matter.

Built on the Insurance Agent App platform by GoInsuranceAgent, a Vertafore Orange Partner.

SOC 2 Type II compliantCyber sits in a portfolio. Here is what sits next to it.

General Liability

Third-party bodily injury and property damage from operations. GL explicitly excludes cyber and electronic data exposures through the Aircraft, Auto, or Watercraft exclusion and the electronic data exclusion. Cyber sits next to GL, not inside it.

Professional Liability (E&O)

Service-business E&O policies sometimes overlap with cyber on technology errors and omissions claims. The IT services E&O market frequently bundles cyber, but the bundling structure and the sub-limits vary widely. McDade audits the overlap.

Business Owners Policy (BOP)

Most Texas BOPs include only a small cyber endorsement, typically 25,000 to 100,000 dollars. Sufficient for initial notification but not for any serious cyber incident given the 120,000 to 1,240,000 dollar realistic SMB breach range. Stand-alone cyber is the answer.

Commercial Crime / Employee Theft

Crime policies cover employee dishonesty and theft of money, securities, and property. Crime does not cover most cyber social engineering scenarios. Social engineering fraud is a cyber endorsement, not a crime endorsement.

Cyber Liability. The twelve questions worth asking.

How long do small businesses survive after a cyber attack?

A serious cyber event can put pressure on revenue, customer trust, contract compliance, privacy duties, and response costs at the same time. The issue is rarely one invoice; it is the stack of business interruption, legal counsel, forensics, notification, vendor recovery, social engineering loss, and contract fallout. Cyber liability insurance does not prevent the attack. It helps fund the recovery plan that keeps the business operating.

What is the Texas Data Privacy and Security Act and how does it affect my business?

The Texas Data Privacy and Security Act (TDPSA) became effective July 1, 2024. The Act applies to businesses that conduct business in Texas or produce products or services consumed by Texas residents, and that meet processing thresholds. The Texas Attorney General has exclusive enforcement authority. Civil penalties can reach 7,500 dollars per violation, with each affected consumer counting as a separate violation. A 30-day cure period applied before January 1, 2025, but expired on that date. The Texas Attorney General filed the first TDPSA lawsuit on January 13, 2025, against Allstate Corporation and five Arity subsidiaries, claiming over 1,000,000 dollars in monetary relief. Investigations now affect over 100 companies. Texas Data Broker Law penalties stack at 100 dollars per day with a 10,000 dollar 12-month maximum and constitute deceptive trade practices under the Texas DTPA. Cyber liability policies typically respond to TDPSA defense and indemnity within the regulatory defense and fines sub-limit.

What does cyber liability insurance actually cover?

Modern cyber liability policies split coverage into first-party and third-party sections. First-party coverage pays your costs after an incident: incident response and forensic investigation, legal counsel, ransom payment (subject to OFAC and carrier approval), business interruption income loss during recovery, system restoration and data recovery, breach notification to affected individuals, credit monitoring for affected individuals, and public relations crisis response. Third-party coverage pays liability arising from the incident: privacy liability for failure to protect personally identifiable information, network security liability for transmission of harmful code or denial-of-service, regulatory defense and fines (including TDPSA penalties to the extent insurable), payment card industry (PCI) fines and assessments, and media liability for content published online. Optional endorsements add social engineering fraud (wire fraud and invoice manipulation), reputational harm, contingent business interruption for vendor outages, and cryptojacking.

What is the average cost of a cyber attack on a Texas small business?

Cyber loss cost varies by incident type, revenue, downtime, data type, payment-card exposure, vendor dependency, and contract obligations. Ransomware, business email compromise, privacy notification, forensic investigation, legal counsel, customer churn, and interrupted operations can stack together quickly. The McDade Cyber Liability Review does not pick a limit from a headline number; it maps first-party and third-party limits to how your business actually operates.

What is the difference between first-party and third-party cyber coverage?

First-party cyber coverage pays your business's own costs after a cyber incident. These include forensic investigation to determine what happened, legal counsel during the incident, ransom payment if you elect to pay and the carrier approves under OFAC restrictions, business interruption income loss while systems are down, system restoration and data recovery, breach notification expense to affected individuals as required by Texas Business and Commerce Code Chapter 521, credit monitoring services for affected individuals, and public relations crisis response. Third-party cyber coverage pays liability from claims brought against your business by others. These include privacy liability lawsuits for failure to protect personally identifiable information, network security liability for transmitting harmful code or causing a denial-of-service condition, regulatory defense and fines (including Texas Attorney General TDPSA actions), Payment Card Industry assessment defense, and media liability for online content. A complete cyber program carries both first-party and third-party limits, often with separate sub-limits per coverage line.

Is ransom payment covered by cyber liability insurance?

Most cyber liability policies include cyber extortion coverage that can fund a ransom payment, subject to carrier consent and U.S. Treasury Office of Foreign Assets Control (OFAC) compliance. OFAC publishes a Specially Designated Nationals list, and any ransom payment to a sanctioned actor or jurisdiction can produce significant federal penalties even where coverage exists. The U.S. Treasury has explicitly warned that paying ransoms to sanctioned actors violates federal law regardless of insurance coverage. Carrier consent is required before payment. The decision to pay or not pay is strategic and rarely simple. Research published in 2025 shows that 69 percent of businesses that paid a ransom were attacked again, and 82 percent who paid received less than the original demand. Many Texas businesses that experience ransomware now choose not to pay because of repeat-attack risk and OFAC complexity, and instead use cyber liability coverage for system restoration and business interruption.

What is social engineering coverage and why does my business need it?

Social engineering coverage, sometimes called funds transfer fraud, social engineering fraud, or computer fraud, covers loss from fraudulent transfer of money or securities caused by deception. Common scenarios include the fake CEO email, the changed vendor invoice, and the fake contract amendment requesting a funds transfer. This coverage is often handled by a specific cyber endorsement or sub-limit, and it may not be handled by crime, general liability, or property policies. McDade checks the wording because social engineering is one of the easiest cyber gaps to miss.

How does the Texas Identity Theft Enforcement and Protection Act apply to my business?

Texas Business and Commerce Code Chapter 521, the Identity Theft Enforcement and Protection Act, requires businesses that own, license, or maintain sensitive personal information about a Texas resident to notify affected individuals as quickly as possible after discovering a security breach involving that information. Notification must occur within 60 days of breach discovery. Notification to the Texas Attorney General is required for breaches affecting 250 or more Texas residents. Penalties include civil penalties up to 50,000 dollars per violation imposed by the Texas Attorney General, plus separate notification cost obligations to affected consumers (typically credit monitoring for one year). Cyber liability policies typically cover the notification process, the credit monitoring expense, and the regulatory defense costs associated with Chapter 521 violations within the privacy regulatory sub-limit.

What is the McDade Cyber Liability Review?

The McDade Cyber Liability Review is an audit of your existing cyber liability policy by Dallas Downey, CLCS, with the McDade commercial team. The review evaluates four primary areas specific to Texas businesses. First, the limit structure across first-party and third-party coverage lines against your operational exposure (annual revenue, employee count, sensitive data volumes, PCI scope). Second, the TDPSA regulatory defense and fines sub-limit against your Texas Attorney General exposure (which now scales at 7,500 dollars per affected consumer). Third, the ransomware and business interruption coverage including the waiting period, the period of indemnity, and the OFAC compliance language. Fourth, the social engineering fraud coverage and the sub-limit, which is the most common Texas commercial cyber gap and the most common Texas commercial cyber loss. About 40 percent of the time the review confirms the current carrier and policy structure are correct. The other 60 percent identifies sub-limit shortfalls, exclusion gaps, or carrier restructuring opportunities.

Why does Charles McDade have a personal connection to cyber risk?

The cyber lineage in Charles's family runs to Houston, 1997. The late Douglas Finley, Charles's grandfather, founded Naknan Inc., a Houston Clear Lake area endpoint security and information technology services company. Naknan operated in Houston's NASA corridor at 1300 Bay Area Boulevard for over two decades, providing endpoint security, patch management, IT services, software engineering, and network security products to commercial and government clients. The flagship product was a security software platform called Security Assistant. Naknan held federal 8(a) Small Disadvantaged Business certification and was minority-owned and woman-owned. Charles grew up understanding that cybersecurity is not abstract, it is what working families build businesses around in Houston. The McDade Cyber Liability Review carries that family understanding of cyber risk into the broker's chair. Cyber liability insurance does not prevent the attack. Cyber liability insurance, paired with appropriate security controls, prevents the closure that follows the attack.

Who handles Cyber Liability at McDade?

Dallas Downey, CLCS leads the McDade commercial insurance team including Cyber Liability. Dallas holds the Certified Lines Coverage Specialist designation and routes commercial conversations through a dedicated commercial meeting calendar. Charles McDade reviews cyber policies alongside Dallas, drawing on the family background in endpoint security and information technology services through Naknan Inc. The McDade office serves the Houston metropolitan area including Spring, Klein, Tomball, Cypress, The Woodlands, Conroe, Humble, Katy, and Bridgeland, plus all of Texas through Premier Group Insurance carrier access including 50+ top Texas carriers we know well. McDade Insurance Brokerage Group is licensed by the Texas Department of Insurance (Texas License 2539471). Schedule a commercial review through the commercial routing on this page or call the McDade office at 281.378.5002.

What cyber coverage limit should a Texas small business carry?

There is no universal correct limit. The starting point is operational exposure measured across annual revenue, employee count, sensitive data records held, PCI cardholder data scope, and contract-required minimums from your largest clients. For Texas small businesses under 50 employees with no PCI scope and limited sensitive data, 1,000,000 dollars combined first-party and third-party is the floor and 3,000,000 dollars is common. For Texas mid-size businesses with 50 to 500 employees, 3,000,000 to 10,000,000 dollars is the typical range. Healthcare, financial services, and any business handling significant PCI or PHI scope typically requires 5,000,000 to 25,000,000 dollars or more. Contract requirements from large general contractors, healthcare facilities, and government clients increasingly mandate specific cyber minimums in the 2,000,000 to 5,000,000 dollar range. The McDade Review evaluates the limit against your specific operational and contract exposure.

Start the conversation

Send the policy. We will read it.

Drop your name, business, phone, and a quick line about what your operation looks like. A licensed Texas broker will follow up within one business day.

What we will ask for next. Your current cyber policy declaration page if you have one. The contract requirement that triggered this conversation if applicable. A rough sense of revenue, employee count, and what kind of data you handle. That is enough to size the right limit.

Send your current cyber declarations. Dallas Downey and Charles McDade audit all four.

The McDade Cyber Liability Review evaluates the first-party and third-party limit structure across all coverage lines, the TDPSA regulatory defense and fines sub-limit against your Texas Attorney General exposure, the ransomware and business interruption coverage including OFAC compliance language, and the social engineering fraud coverage and sub-limit. Dallas Downey, CLCS leads the commercial review. Charles McDade reviews cyber policies alongside Dallas. Most reviews complete inside one business week. About 40 percent of the time the audit confirms the current structure is correct. The other 60 percent identifies sub-limit shortfalls, exclusion gaps, or carrier restructuring opportunities.

Back to the commercial hub. Houston Business Insurance

Or call 281.378.5002

The review is advisory. McDade is licensed by the Texas Department of Insurance (Texas License 2539471).